Build Your HOA Website Free

Running an HOA is a big job for a volunteer.

Neighborhood.online gives your community a modern website, document storage, and communication tools in minutes.

No technical skills required.

HOA Cybersecurity Insurance

- The Coverage Gap Most HOAs Do Not Know They Have

- Why HOAs Are a Target

- What HOA Cyber Liability Insurance Covers

- What Your General Liability Policy Does Not Cover

- What the Data Shows About HOA Cybersecurity

- The Most Common Threats Facing HOA Boards

- What Boards Should Do Before a Breach Happens

- Choosing Cyber Liability Coverage

- Action Steps for Your Board

Keep Your Whole Community in the Loop

Homeowners trust boards that communicate clearly. A free Neighborhood.online website makes it easy to share meeting minutes, post updates, and give residents one place to find everything they need.

Build Your Free HOA WebsiteMost HOA boards would not dream of operating without general liability or property insurance. But when it comes to cybersecurity, many of the same boards are running entirely unprotected. They collect dues online, store resident data in management software, send communications by email, and conduct financial transactions electronically. And most have no coverage if any of those systems are compromised.

According to the Foundation for Community Association Research's 2025 Insurance Coverage Trends Snap Survey of 509 respondents across 39 states, 33% of HOAs do not carry any cybersecurity insurance. That is one in three communities with real digital exposure and no financial protection if something goes wrong. A data breach, a ransomware attack, or a fraudulent wire transfer can generate costs that a community's general liability policy will not touch and that reserves were not designed to absorb.

This article explains what cyber liability insurance covers, why HOAs need it, and what boards should do to reduce their exposure before a breach happens.

The Coverage Gap Most HOAs Do Not Know They Have

There is a common and dangerous assumption among HOA boards that their general liability or property insurance covers cyber incidents. It does not. Standard general liability policies explicitly exclude cyber incidents, and property policies cover physical assets, not digital ones. A ransomware attack that locks your management software, a phishing scam that diverts an assessment payment, or a data breach that exposes resident personal information all fall entirely outside the coverage most HOAs carry.

The financial consequences of a cyber incident can be significant. Direct costs include forensic investigation, legal notification to affected residents, credit monitoring services for affected parties, regulatory fines where applicable, and the cost of restoring systems and data. Indirect costs include the board's time, reputational damage, and the potential for resident claims. None of this is covered by general liability or property insurance.

Cyber liability insurance exists specifically to fill this gap. It is the policy that responds when a digital system is compromised and the HOA has financial obligations as a result.

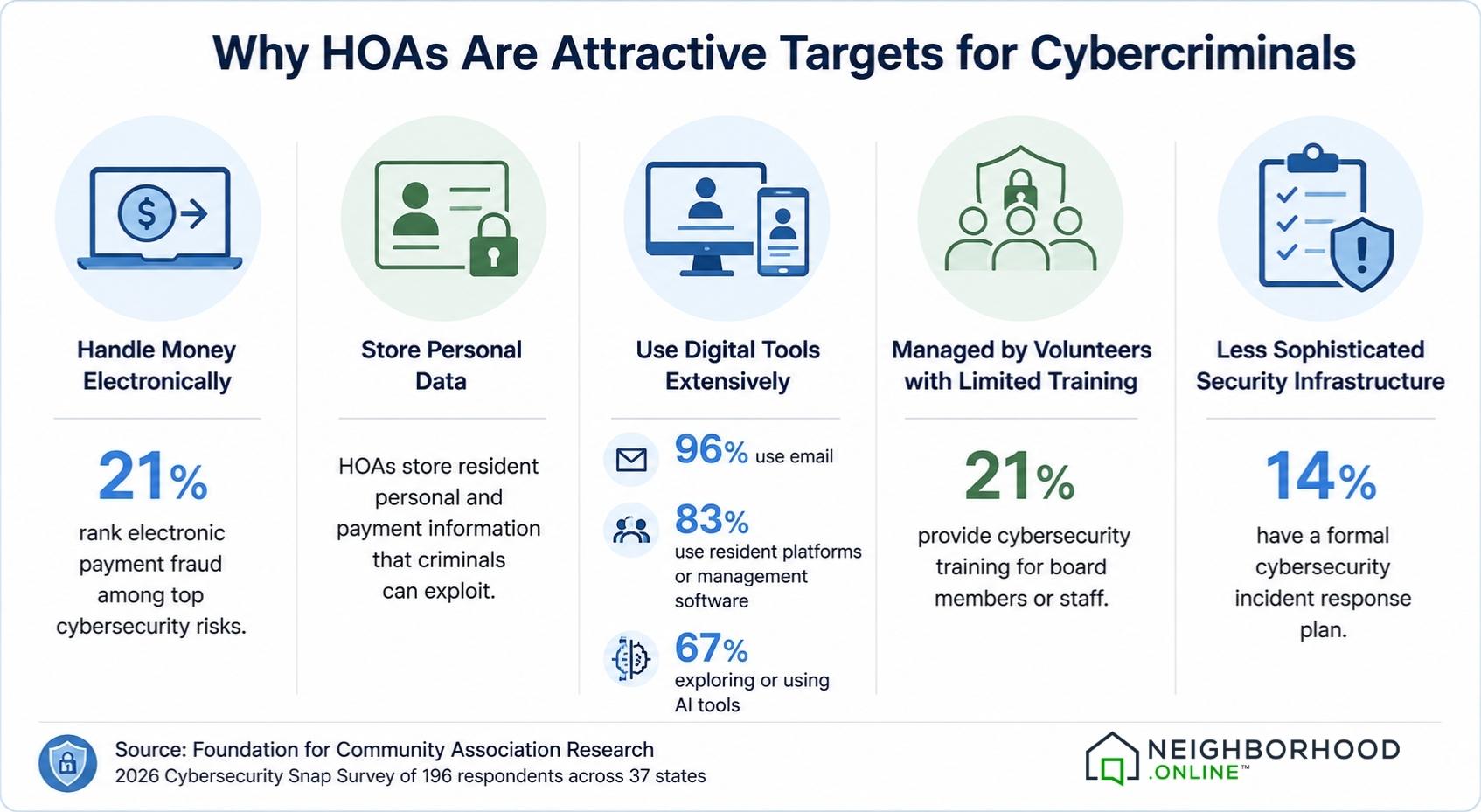

Why HOAs Are a Target

HOAs are not large corporations, but they share several characteristics that make them attractive targets for cybercriminals.

They handle money electronically. HOAs collect assessments, pay vendors, and manage reserve funds. A fraudulent wire transfer or ACH diversion can move significant sums before anyone notices. According to the Foundation for Community Association Research's 2026 Cybersecurity Snap Survey of 196 respondents across 37 states, 21% of HOAs rank electronic payment fraud among their top cybersecurity risks.

They store personal data. HOA management systems hold resident names, addresses, email addresses, phone numbers, payment information, and sometimes more. That data has value to criminals, and HOAs that hold it have legal obligations when it is breached.

They use digital tools extensively. The same 2026 survey found that 96% of HOAs use email to communicate with residents, 83% use resident platforms or management software, and 67% are exploring or using AI tools. Every digital touchpoint is a potential entry point for a bad actor.

They are often managed by volunteers with limited security training. Only 21% of HOA communities provide cybersecurity training for board members or staff, according to the 2026 survey. Boards that handle sensitive information without formal security practices are more vulnerable to phishing, social engineering, and accidental data exposure than organizations with dedicated IT staff.

They typically have less sophisticated security infrastructure. Only 14% of communities have a formal cybersecurity incident response plan. When a breach occurs, a board without a response plan takes longer to contain the damage, which increases both the cost and the scope of the incident.

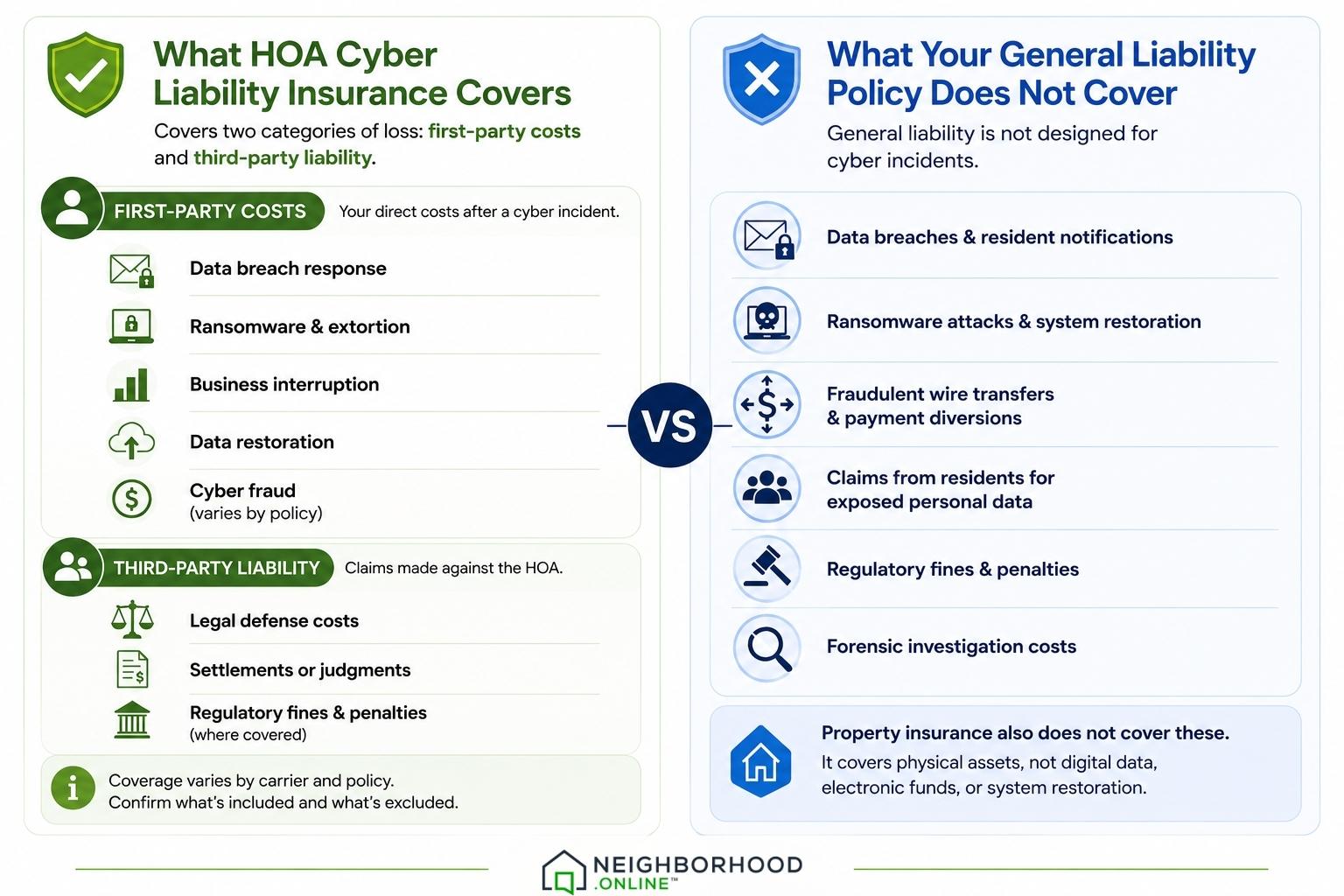

What HOA Cyber Liability Insurance Covers

Cyber liability insurance for HOAs typically covers two categories of loss: first-party costs and third-party liability.

First-party costs are the direct expenses the HOA incurs as a result of a cyber incident:

- Data breach response: The cost of investigating the breach, notifying affected residents, and providing credit monitoring or identity theft protection services to those whose data was compromised

- Ransomware and extortion: Costs associated with responding to a ransomware attack, including negotiation and, in some cases, ransom payments where legally permitted

- Business interruption: Revenue loss or additional expenses incurred while systems are down or compromised

- Data restoration: The cost of recovering or recreating data that was destroyed, corrupted, or stolen

- Cyber fraud: Some policies cover financial losses from fraudulent wire transfers or electronic payment fraud, though this varies by policy and should be confirmed with your agent

Third-party liability covers claims made against the HOA by residents, vendors, or others who were harmed by the breach:

- Legal defense costs if a resident sues the HOA over a data breach that exposed their personal information

- Settlements or judgments arising from third-party claims related to the breach

- Regulatory fines and penalties where covered under the policy

Not all cyber liability policies cover all of these categories. Coverage varies significantly by carrier and policy structure. When evaluating options, confirm specifically what first-party and third-party coverages are included and what the exclusions are.

What Your General Liability Policy Does Not Cover

It is worth being explicit about this because the assumption that general liability covers cyber incidents is one of the most common and costly gaps in HOA insurance programs.

Your HOA's general liability policy covers bodily injury, property damage, and related legal liability arising from physical incidents in common areas. It does not cover:

- Data breaches or the cost of notifying affected residents

- Ransomware attacks or the cost of restoring encrypted systems

- Fraudulent wire transfers or electronic payment diversions

- Claims from residents whose personal data was exposed

- Regulatory fines for data protection violations

- The cost of forensic investigation after a digital incident

Your property insurance policy also does not cover these losses. Property insurance covers physical assets. Digital data, electronic funds, and system restoration costs are not physical assets in the way your policy is written.

For a complete picture of what your HOA's general liability policy covers and where its limits are, see our post on HOA general liability insurance.

What the Data Shows About HOA Cybersecurity

Two recent surveys from the Foundation for Community Association Research paint a clear picture of where HOAs stand on cybersecurity. The findings are worth understanding because they describe the conditions under which a breach is most likely to occur and be costly.

From the 2026 Cybersecurity in Community Associations Snap Survey (196 respondents, 37 states):

- 54% of HOA communities do not have formal cybersecurity policies and procedures in place

- 25% report experiencing at least one cybersecurity incident in the past three years

- Only 51% carry cyber liability or data breach insurance coverage

- Only 14% have a formal cybersecurity incident response plan

- Only 21% provide cybersecurity training for board members or staff

- Only 21% evaluate cybersecurity practices when selecting vendors or technology providers

From the 2025 Insurance Coverage Trends Snap Survey (509 respondents, 39 states):

- 33% of HOAs do not carry cybersecurity insurance at all

- 57% of communities that do carry cyber insurance saw their premiums increase in 2024

- 5% had their cyber policy non-renewed or canceled by the insurer

Taken together, these figures describe a community association sector that is increasingly digital, increasingly targeted, and still significantly under-prepared and under-insured for the cyber risks it faces.

Source: Foundation for Community Association Research. (2025, April). Insurance coverage trends in community associations [Snap survey]. Community Associations Institute. Foundation for Community Association Research. (2026, April). Cybersecurity in community associations [Snap survey]. Community Associations Institute.

Not sure if your HOA has the right coverage?

The HOA Insurance Review Checklist walks your board through every policy type including cyber liability, coverage limits, exclusions, and vendor requirements in one annual review. Free in PDF and Word.

Download Free ChecklistThe Most Common Threats Facing HOA Boards

Understanding the specific threats HOAs face helps boards make better decisions about both coverage and prevention. The 2026 Cybersecurity Snap Survey identified the following as the top risks facing communities today.

Phishing scams targeting board members, managers, or residents were ranked as the top cybersecurity risk by 38% of respondents. Phishing emails impersonate trusted contacts, including vendors, banks, or other board members, to trick recipients into revealing credentials, approving fraudulent payments, or clicking links that install malware. The survey noted that AI is now being used to impersonate vendors and homeowners with increasing sophistication, making these attacks harder to detect.

Fraud and theft of association funds was identified by 28% of respondents as a top risk. This includes fraudulent wire transfer requests, ACH diversion schemes, and check fraud. Electronic payment fraud was specifically identified by 21% as a top concern. These attacks often begin with a phishing email that compromises a board member's or manager's email account, then uses that access to redirect legitimate payment instructions.

Management software and system breaches were cited by 26% of respondents. With 83% of HOAs using resident platforms or management software, a breach of the platform itself or of the HOA's account within the platform can expose resident data, financial records, and communication histories.

Resident data exposure was identified by 23% as a top risk. HOAs hold personally identifiable information about every homeowner in the community. A breach that exposes that data creates notification obligations, potential liability, and reputational damage regardless of how the breach occurred.

Ransomware attacks were identified by 23% of respondents. Ransomware encrypts an organization's data and systems and demands payment for restoration. For an HOA that loses access to its management software, financial records, and communication systems, the operational disruption alone can be significant before any ransom consideration is involved.

What Boards Should Do Before a Breach Happens

Cyber liability insurance is the financial backstop when something goes wrong. It is not a substitute for the practices that reduce the likelihood of an incident in the first place. The 2026 survey found that 75% of HOA respondents believe training and education would most help reduce cybersecurity risk, and 68% identified clear policies and best practices as important tools. The gap between what boards know they need and what they have in place is significant.

The most impactful steps a board can take before a breach are also the most straightforward.

Use strong, unique passwords and multi-factor authentication. The 2026 survey found that 52% of communities use multi-factor authentication. That means nearly half do not. Enabling multi-factor authentication on every account that accesses financial systems, management software, or email is one of the single most effective defenses against unauthorized access and costs nothing to implement.

Establish a payment verification process. Any request to change banking information or redirect a payment should require verbal confirmation with a known contact at a known number before being processed. Never rely on email alone to verify a payment change. This single practice prevents the majority of wire transfer fraud incidents.

Train board members and staff to recognize phishing. Only 21% of communities provide cybersecurity training. A basic annual training session covering how to identify phishing emails, what to do when something looks suspicious, and how to report a potential incident is low cost and high impact. Most insurance carriers that offer cyber liability coverage can provide or point to training resources.

Have a written incident response plan. Only 14% of HOA communities have one. An incident response plan does not need to be complex. It needs to answer four questions: who is notified first when a breach is suspected, who has authority to take action, what are the immediate containment steps, and who are the external resources (insurance carrier, legal counsel, IT support) to contact. A plan completed before an incident means faster response and lower total cost.

Vet the cybersecurity practices of vendors and software providers. Only 21% of HOAs evaluate cybersecurity when selecting vendors. If your management software provider or payment processor experiences a breach, your resident data may be compromised regardless of your own practices. Ask vendors about their security certifications, data encryption practices, and breach notification procedures before committing to a platform.

Choosing Cyber Liability Coverage

Cyber liability insurance for HOAs has become more standardized in recent years, but policies still vary significantly in what they cover, what they exclude, and how claims are handled. When evaluating options, work with an insurance agent who has experience placing cyber coverage for community associations rather than a general commercial agent who may not be familiar with HOA-specific risks.

Key questions to answer when evaluating a cyber liability policy:

- Does the policy cover first-party costs including breach response, notification, and data restoration?

- Does it cover ransomware and extortion payments?

- Does it cover electronic payment fraud and wire transfer fraud specifically?

- What are the coverage limits and are they adequate for the size of your community and the volume of financial transactions you process?

- What is the deductible and can your reserves absorb it?

- Does the policy include access to breach response services such as forensic investigation and legal notification support?

- What are the exclusions and do any of them apply to the most likely threats your community faces?

- What does the policy require you to have in place in terms of security practices? Some policies require multi-factor authentication or other controls as a condition of coverage.

The cost of cyber liability coverage has increased alongside claims frequency, as reflected in the 57% of communities that saw premium increases in 2024. Even at higher premiums, the coverage is typically modest in cost relative to the potential losses it covers. A forensic investigation and resident notification program for even a small data breach can run tens of thousands of dollars. Coverage that costs a few hundred to a few thousand dollars annually is a reasonable investment for most communities.

For more on the technology tools HOA boards can use to reduce risk and improve documentation, see our post on technology tools that support HOA operations. For a complete overview of every insurance type your board should carry, see our guide to HOA risk and insurance essentials.

Action Steps for Your Board

- Confirm whether your HOA currently carries any cyber liability or data breach insurance coverage

- If you do not carry it, ask your insurance agent for a quote and confirm what first-party and third-party coverages are included

- If you do carry it, review the coverage limits, exclusions, and deductible at your next renewal

- Confirm that your general liability policy explicitly excludes cyber incidents so your board understands the gap

- Enable multi-factor authentication on every account that accesses financial systems, management software, or board email

- Establish a written payment verification process that requires verbal confirmation before any banking information change is processed

- Schedule a basic cybersecurity training session for board members before the end of the year

- Write a one-page incident response plan that names who to call first and what immediate steps to take if a breach is suspected

- Review the cybersecurity practices of your management software and payment processing vendors

- Add cyber liability coverage to your annual HOA Insurance Review Checklist so it is evaluated at every renewal

Free Download: HOA Insurance Review Checklist

The coverage review section of this checklist includes cyber liability insurance so your board evaluates it at every annual renewal alongside every other policy type. 49 items across 6 sections, free in PDF and Word.

Download Free ChecklistSources

Foundation for Community Association Research. (2026, April). Cybersecurity in community associations [Snap survey]. Community Associations Institute. https://foundation.caionline.org/wp-content/uploads/2026/05/Snap-Survey-Cybersecurity.pdf

Foundation for Community Association Research. (2025, April). Insurance coverage trends in community associations [Snap survey]. Community Associations Institute. https://foundation.caionline.org/wp-content/uploads/2023/04/4ppInsuranceSnapSurvey.pdf

Updated June 25, 2026

- The Coverage Gap Most HOAs Do Not Know They Have

- Why HOAs Are a Target

- What HOA Cyber Liability Insurance Covers

- What Your General Liability Policy Does Not Cover

- What the Data Shows About HOA Cybersecurity

- The Most Common Threats Facing HOA Boards

- What Boards Should Do Before a Breach Happens

- Choosing Cyber Liability Coverage

- Action Steps for Your Board