Build Your HOA Website Free

Running an HOA is a big job for a volunteer.

Neighborhood.online gives your community a modern website, document storage, and communication tools in minutes.

No technical skills required.

Are HOA Dues Tax Deductible?

Keep Your Whole Community in the Loop

Homeowners trust boards that communicate clearly. A free Neighborhood.online website makes it easy to share meeting minutes, post updates, and give residents one place to find everything they need.

Build Your Free HOA WebsiteUpdated June 30, 2026

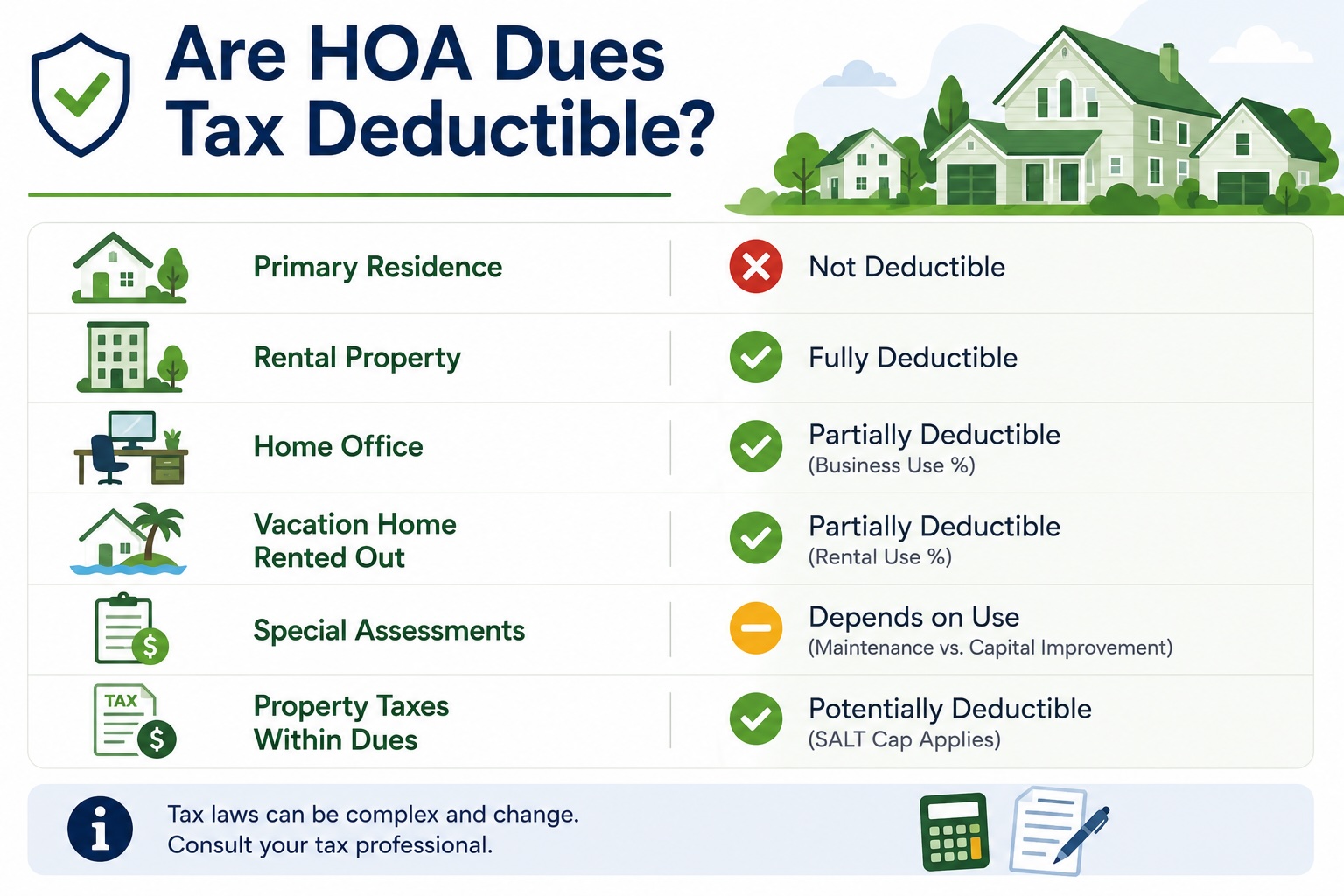

For most homeowners, HOA dues are not tax deductible. The IRS treats them as a personal expense, the same as your utility bills or grocery runs, and personal expenses do not qualify for a federal deduction. But there are three situations where the answer changes, and if you fall into one of them, the deduction can be meaningful. This post covers all of it plainly so you know where you stand before tax season.

This is general information, not tax advice. Your specific situation depends on how you use the property, your income, and current tax law. A CPA or tax professional can confirm what applies to you.

Why HOA Dues Are Not Deductible for Most Homeowners

The IRS defines deductible expenses as those that are either business-related or specifically authorized by tax law. HOA dues paid on a primary residence are neither. They fund maintenance and operations for your neighborhood, which counts as a personal benefit rather than a business cost.

This surprises some homeowners because property taxes are deductible (up to the $10,000 SALT cap), and both property taxes and HOA dues show up as ongoing costs of owning a home. But the IRS treats them differently. Property taxes are a government levy that qualifies for a specific deduction. HOA dues are a private contractual obligation to your association, and no equivalent deduction exists for them.

The same rule applies to most HOA-related costs, including fines, late fees, and administrative charges. None of these are deductible for a primary residence.

When HOA Dues Are Tax Deductible

There are three scenarios where HOA dues can become deductible, fully or in part. Each one depends on how you use the property.

Rental properties. If you rent out your home or condo, HOA dues are fully deductible as a business expense. The IRS considers rental properties a business activity, and HOA dues are an ordinary and necessary cost of running that business. You report them on Schedule E along with your other rental expenses. This applies whether you rent the property full-time or use it as a long-term rental. If you rented out your property for any portion of the year, only the dues attributable to the rental period are deductible.

Home office deduction. If you work from home and qualify for the IRS home office deduction, you may be able to deduct a proportional share of your HOA dues. The deduction is calculated based on the percentage of your home used exclusively and regularly for business. If your home office is 10 percent of your home's square footage, roughly 10 percent of your HOA dues may be deductible. The home office must meet the IRS definition of exclusive business use, meaning the space cannot double as a guest room or personal space.

Vacation or second homes rented to others. If you own a vacation home and rent it out for more than 14 days per year, a portion of your HOA dues may be deductible. The deductible share is calculated based on the ratio of rental days to total days of use during the year. If you use the home yourself for 30 days and rent it for 90 days, roughly 75 percent of the HOA dues for that year may be deductible as a rental expense.

In all three cases, the logic is the same: the deduction is available when the property is being used to generate income, not when it is being used for personal enjoyment.

Are HOA Special Assessments Tax Deductible?

Special assessments follow similar rules to regular dues, with one additional consideration. For a primary residence, special assessments are generally not deductible regardless of what they fund.

For a rental property, it depends on what the assessment is for. If the assessment covers routine maintenance or repairs (repaving the parking lot, replacing pool equipment), it may be deductible as a rental expense in the year it is paid. If the assessment funds a capital improvement that adds value to the property (a new roof on the building, a major structural upgrade), it is typically not immediately deductible. Instead, it increases your property's cost basis, which affects the gain calculation when you eventually sell.

This distinction matters because capital improvements and maintenance expenses are treated very differently under tax law. If your HOA issues a large special assessment, it is worth asking the board whether it is for maintenance or capital improvement before you file, because the answer changes how you handle it on your return.

What if My HOA Dues Include Property Taxes?

Some HOA communities, particularly older planned developments, collect property taxes as part of the monthly dues and remit them on behalf of homeowners. If your dues include a property tax component, that portion may still be deductible as a property tax payment, subject to the $10,000 SALT deduction cap.

The key is documentation. Your HOA needs to provide a clear breakdown showing exactly how much of your dues went toward property taxes versus maintenance, reserves, and management. Without that breakdown, the IRS has no basis to allow the deduction. You can request an itemized breakdown of your dues from your board or management company. Understanding operating and reserve funds will help you read that breakdown once you have it.

Does It Matter What HOA Dues Pay For?

No. The deductibility of HOA dues is determined by how you use the property, not by what the dues fund. Even if your HOA uses every dollar on landscaping, security, and amenities you genuinely value, those dues are still a personal expense if the property is your primary residence.

For anyone curious about what HOA dues actually cover, that is a separate question from deductibility, and understanding how HOA budgets work can help homeowners evaluate whether their dues are reasonable regardless of the tax treatment.

A Quick Summary

- Primary residence: HOA dues are not tax deductible.

- Rental property: HOA dues are fully deductible as a business expense for the rental period.

- Home office: The business-use percentage of HOA dues may be deductible if you qualify for the home office deduction.

- Vacation home rented out: The rental-use percentage of HOA dues may be deductible.

- Special assessments: Not deductible for personal residences. For rental properties, deductibility depends on whether the assessment is for maintenance or a capital improvement.

- Property taxes within dues: The property tax portion may be deductible if properly documented, subject to the $10,000 SALT cap.

How to Keep Records That Support a Deduction

If you rent your property or have a home office, keeping clean records of your HOA dues is worth the small effort. Save your HOA payment confirmations or bank statements showing each payment. If you receive an annual statement from your HOA, keep that as well. For rental properties, your dues are just one of several expense categories you will need to document on Schedule E, and having a clear record makes the filing straightforward.

If your community uses a management platform or member portal, payment history is usually available in your account anytime you need it. Neighborhood.online, for example, keeps a record of dues payments that homeowners can access directly, which simplifies the documentation process at tax time without having to chase down statements from the board.

The Bottom Line

If you own your home and live in it, HOA dues are almost certainly not deductible on your federal return. If you rent it out, run a qualifying home office, or own a vacation home that you also rent to others, part or all of your dues may be deductible. The specific rules depend on your situation, and tax law does change, so confirming with a CPA before you file is the safest move if any of the exceptions apply to you.

If you want simple, modern, and free to start, you are in the right place.

We run your community.

Set up a complete community platform in under an hour. No developer required. No credit card needed. No accounting degree required.