Special Assessments

Why They Happen, How Much They Cost & How to Prevent Them

Special Assessments

Few things cause more tension in an HOA community than a special assessment notice. Homeowners open the letter, see an unexpected charge, and the board suddenly has a lot of explaining to do.

The frustrating part is that most special assessments are preventable. Not all of them, but most. Understanding why they happen is the first step toward making sure your community isn't caught off guard by one.

What Is a Special Assessment?

A special assessment is a one-time charge levied on homeowners outside of regular dues. It's used to cover a cost that the HOA's regular budget and reserve fund can't absorb on their own.

Unlike monthly dues, which are predictable and budgeted in advance, a special assessment usually arrives with little warning and a tight payment deadline. Amounts can range from a few hundred dollars to several thousand per homeowner, depending on the size of the community and the expense being covered.

Most HOA governing documents give the board authority to issue special assessments up to a certain amount without a homeowner vote. Above that threshold, a majority vote is typically required. If your board has never reviewed those limits in your CC&Rs or bylaws, now is a good time to do that.

Why Do Special Assessments Happen?

There are a few common causes, and they don't all point to mismanagement.

Underfunded Reserves

This is the most common reason. When an HOA hasn't been setting aside enough money each year to cover future repairs, eventually a major expense arrives and the reserves simply aren't there. A roof replacement, repaving the parking lot, or replacing a failing elevator can cost tens of thousands of dollars. If the reserve account is short, a special assessment fills the gap.

The fix is consistent, adequately funded reserve contributions based on a current reserve study. Our guide on operating vs reserve funds explains how to keep those accounts healthy year over year.

A Genuinely Unexpected Expense

Sometimes a special assessment isn't the result of poor planning. A major storm, a pipe failure inside a shared wall, a legal judgment against the HOA, or a sudden insurance gap can all create costs that no reserve fund could have anticipated.

These situations are harder to prevent entirely, but having a contingency line in your operating budget and carrying adequate insurance coverage reduces the chance that one bad event becomes a financial crisis.

Deferred Maintenance Catching Up

Boards sometimes put off repairs to avoid raising dues or dipping into reserves. It feels like the responsible choice in the short term, but deferred maintenance compounds over time. A small crack in a retaining wall becomes a structural problem. A slow roof leak becomes interior damage. The cost of waiting almost always exceeds the cost of addressing things early.

Reviewing warning signs in your financials regularly can help boards catch these patterns before they become expensive.

A Spike in Operating Costs

Significant increases in insurance premiums, utility rates, or vendor contracts can push an operating budget into deficit if dues weren't adjusted to keep pace. When the operating fund runs short, a special assessment sometimes becomes the only option to cover the shortfall without cutting critical services.

This is one of the strongest arguments for modest, consistent annual dues increases rather than holding dues flat for years at a time. A small adjustment every year is much easier for homeowners to absorb than a large correction or a surprise charge.

How Much Do Special Assessments Typically Cost?

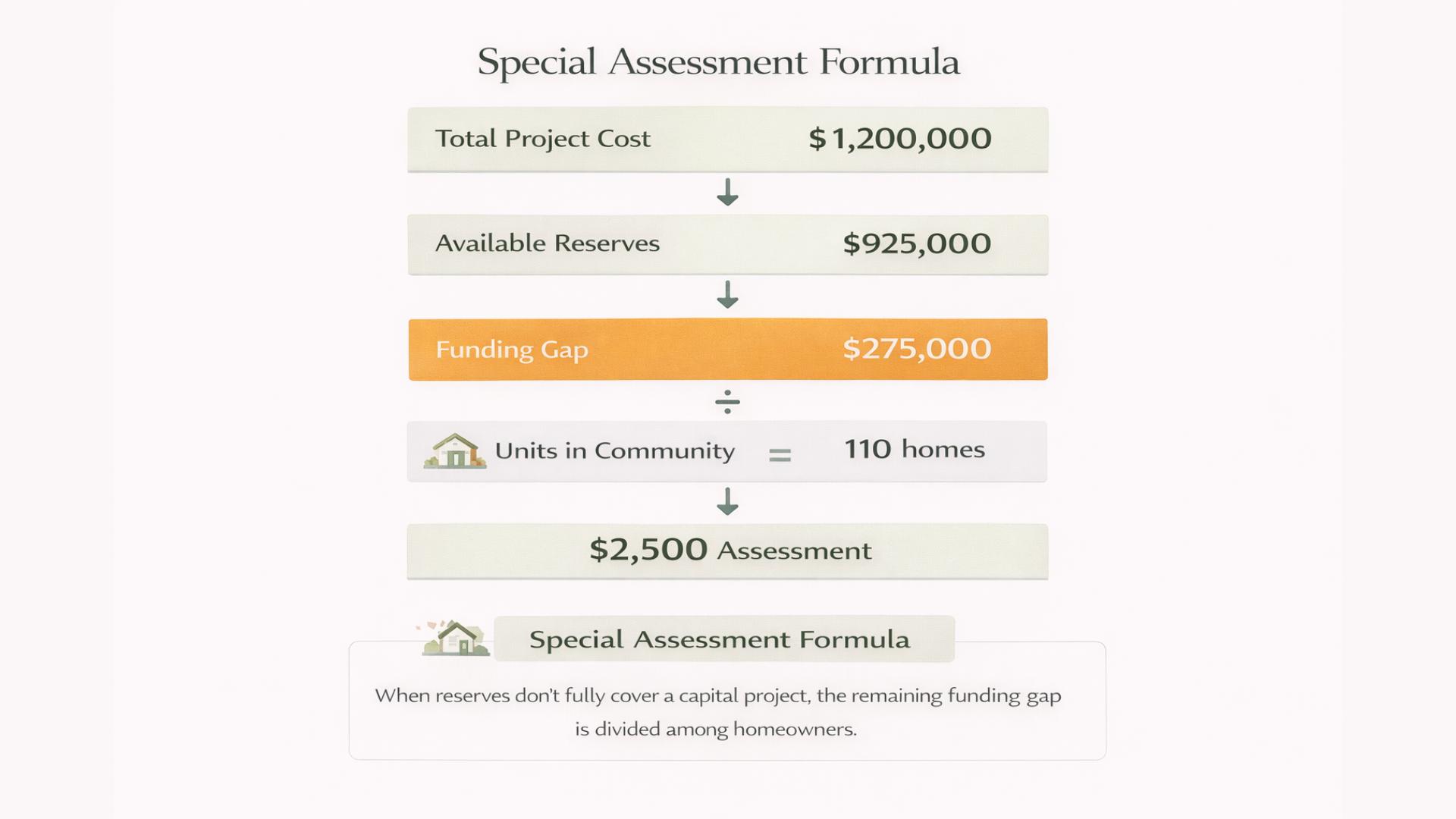

There's no fixed amount. The charge per homeowner depends on the total cost of the expense, divided across the number of units in the community (sometimes weighted by unit size or ownership percentage as defined in the governing documents).

For smaller communities dealing with a moderate repair, a special assessment might be $300 to $500 per homeowner. For larger projects in bigger communities, such as a full roof replacement on a condo building or major infrastructure work, it can run $2,000 to $10,000 or more per unit.

Some HOAs offer payment plans to ease the burden, especially for larger amounts. This is worth discussing with your board and legal counsel before issuing the notice, since the structure of payment options may be governed by your bylaws.

Understanding Special Assessments

Special assessments often feel sudden and confusing to homeowners. In reality, they usually come from predictable financial gaps.

Our Special Assessments Explainer breaks down what causes them, how they’re calculated, and how communities can avoid them with better planning.

How to Communicate a Special Assessment

How the board communicates a special assessment matters almost as much as the assessment itself. Homeowners who feel blindsided or kept in the dark are far more likely to push back, delay payment, or escalate to legal action.

A clear, honest notice should explain what the expense is, why it wasn't covered by regular reserves or the operating budget, how the per-unit amount was calculated, when payment is due, and whether a payment plan is available. The tone should be direct but respectful. Acknowledging that this is a difficult ask goes a long way.

If you need a starting point for the letter itself, this HOA assessment fees letter template is a practical resource for getting the communication right.

How to Prevent Special Assessments

Prevention comes down to a few consistent habits.

Get a reserve study and use it. A reserve study tells you exactly what your major components are, when they'll need repair or replacement, and how much you should be contributing each year to have the money ready. It removes the guesswork from reserve planning and gives the board a defensible basis for its funding decisions.

Review your budget honestly every year. That means using real vendor quotes, not last year's numbers with a small adjustment. It means accounting for insurance increases, inflation on supplies, and any known changes to the community's needs. The financial management guide for community associations covers how to build a budget that actually holds up.

Raise dues incrementally rather than holding them flat. A 3 to 4% annual increase is far less disruptive than a 15% jump or a surprise special assessment. Boards that explain the reasoning behind dues increases, especially by showing homeowners where the money goes, tend to get a lot more cooperation than those who change fees without context. The HOA dues letter template can help you frame that conversation well.

Don't defer maintenance. Address repairs when they come up, not after they've grown into bigger problems. A regular inspection schedule for common areas and major components helps the board stay ahead of the curve.

Build a contingency into your operating budget. Even a modest buffer of 5 to 10% gives the board room to handle small surprises without a special assessment or an emergency board meeting.

If You're Facing One Now

If your HOA is already in a position where a special assessment looks unavoidable, the most important thing is to communicate early and clearly. Don't wait until the last minute to notify homeowners. Give them as much lead time as possible, offer payment options if your governing documents allow, and be honest about what happened and what the board is doing to prevent it from happening again.

Transparency doesn't make the charge disappear, but it does protect the board's credibility and makes the process significantly smoother. Your treasurer report is a good tool for laying out the financial picture clearly so homeowners can see exactly where things stand.

The Bottom Line

Special assessments aren't always a sign of failure. Sometimes unexpected things happen, and a well-run board handles them transparently and efficiently. But the boards that rarely (or never) need to issue one tend to share a few things in common: they fund reserves adequately, adjust dues consistently, stay on top of maintenance, and review their finances throughout the year, not just at budget time.

If you want to strengthen your board's overall financial practices, the complete guide to financial management for community associations is a solid place to start.