Build Your HOA Website Free

Neighborhood.online gives your community a modern website, document storage, and communication tools in minutes. No technical skills required.

How Much Should Your HOA Have in Reserves?

It's one of the most common questions HOA board members ask, and one of the least clearly answered: how much money should actually be sitting in our reserve fund?

The honest answer is that it depends. But "it depends" isn't a plan. This article walks through the framework boards and homeowners use to evaluate reserve health, what lenders and buyers look for, and what underfunded reserves actually cost a community over time.

If you haven't read our overview of how reserve studies work, that's a good place to start. This article picks up where that one leaves off.

The Concept of Percent Funded

The most widely used measure of reserve health is called percent funded. It's a straightforward ratio that compares what your HOA currently has in reserves to what it should theoretically have, given the age and condition of your community's components.

Here's the simplest way to think about it. Imagine your HOA is responsible for a roof that has a 30-year lifespan and will cost $90,000 to replace. If that roof is 15 years old, your HOA is halfway through its useful life. In theory, you should have set aside roughly $45,000 toward that eventual replacement. If you only have $22,500 saved, you're about 50% funded for that component.

A reserve study calculates this across every major component your HOA owns, adds it all up, and produces a single percent funded figure that represents the overall health of your reserves relative to where they should be.

The math behind a full reserve study is more nuanced than this, accounting for interest earned on reserves, inflation in replacement costs, and the timing of multiple overlapping projects. But the underlying concept is always the same: how does what you have compare to what you should have?

What a Healthy Reserve Funding Level Looks Like

The industry standard benchmark, widely used by reserve specialists and community association professionals, breaks down roughly like this.

A percent funded of 70% or higher is generally considered strong. At this level, the HOA has sufficient reserves to handle anticipated replacements without resorting to special assessments or loans. Dues increases, when needed, tend to be gradual rather than jarring.

A percent funded between 30% and 70% is considered fair. The HOA is not in crisis, but there is a funding gap that needs attention. Boards in this range should have a clear plan to increase contributions over time and should be transparent with homeowners about where things stand.

A percent funded below 30% is considered poor or critically underfunded. At this level, the risk of a special assessment is high. Major repairs may get deferred because the money simply isn't there, and deferred maintenance tends to turn into larger, more expensive problems. If your HOA is in this range, it's worth reviewing how special assessments work so the board is prepared for what might be ahead.

It's worth noting that 100% funded is not necessarily the goal. Most reserve professionals consider anything above 70% to be a well-managed community. The objective is a stable, predictable funding trajectory, not a perfect number on a single date.

Why These Numbers Are Not One-Size-Fits-All

Percent funded is a useful benchmark, but it doesn't tell the whole story on its own. Two HOAs could both be at 60% funded and be in very different situations depending on what's coming up in their replacement schedule.

An HOA that is 60% funded with no major replacements due in the next ten years is in a comfortable position. An HOA that is 60% funded with a $200,000 parking lot repaving project due in two years has a real problem. The percent funded figure is always more meaningful when you look at it alongside the upcoming projects section of your reserve study.

The age of your community also matters. Brand new communities often start with low percent funded figures simply because they haven't had time to accumulate reserves. That's expected. What matters is whether the contribution rate is set correctly from the beginning so the community doesn't fall further behind as it ages.

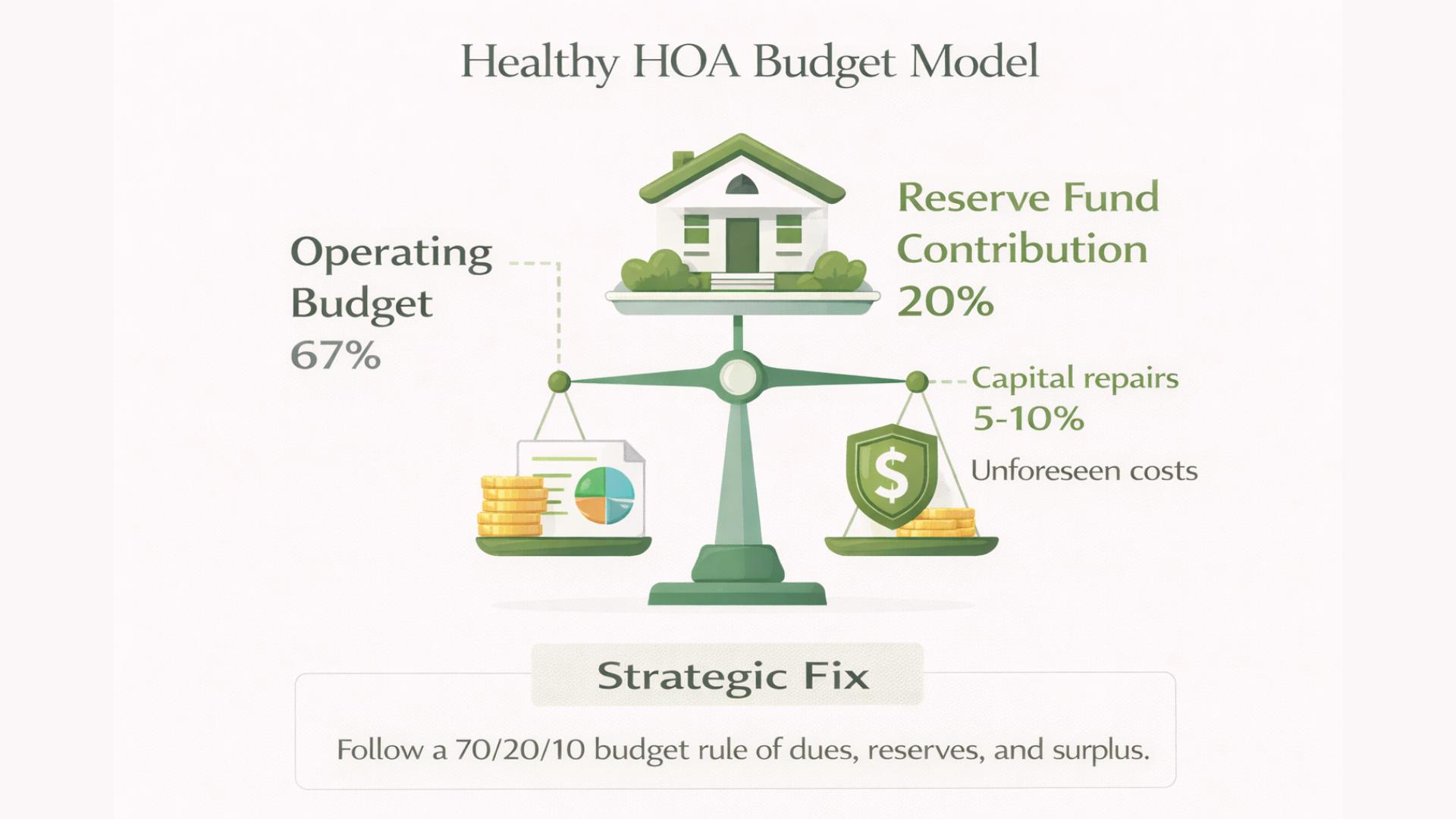

Understanding the relationship between operating and reserve funds is part of building a complete financial picture. Many boards that appear to have healthy operating budgets are quietly underfunding reserves, which shifts the problem rather than solving it.

What Lenders Look For

Reserve health isn't just an internal concern. It directly affects a buyer's ability to get financing in your community, which affects demand for homes and ultimately property values.

Fannie Mae and Freddie Mac, which back the majority of conventional mortgages in the United States, have guidelines around HOA financial health for condominium associations. One key requirement is that the HOA must have at least 10% of its annual budget allocated to reserves. Communities that fall short of this threshold can be flagged as non-warrantable, meaning lenders may decline to offer conventional financing to buyers in that community.

FHA loans have similar requirements. An FHA-approved condominium project must demonstrate adequate reserve funding as part of the approval process. If your community loses FHA approval due to underfunded reserves, it eliminates a significant pool of potential buyers, particularly first-time buyers and those using government-backed loans.

For single-family HOAs, lender scrutiny around reserves is less formalized but still present. Sophisticated buyers and their agents increasingly review reserve study documents and HOA financial statements before closing. A community with visibly underfunded reserves can slow sales and create negotiating leverage for buyers to push prices down.

How Underfunded Reserves Affect Property Values

The connection between reserve health and property values is more direct than most homeowners realize, and it works through several channels at once.

The most immediate impact is buyer perception. When a prospective buyer's agent pulls the HOA's financials and sees a percent funded of 18% with a major roof replacement due in three years, that's a red flag. It signals either a special assessment coming or deferred maintenance ahead. Neither is appealing to a buyer who is about to take on a thirty-year mortgage.

The second channel is actual physical condition. Communities that consistently underfund reserves tend to defer maintenance. Deferred maintenance becomes visible over time. Paint that hasn't been refreshed, parking lots with cracks spreading across them, pool equipment held together with temporary fixes. These things affect how a neighborhood looks and feels, and that affects what buyers are willing to pay.

The third channel is the special assessment risk itself. If a community has issued a special assessment recently, or if one appears likely based on the reserve study, that information travels. Buyers talk to neighbors. Real estate agents remember communities that have had financial problems. A reputation for poor financial management is difficult to shake and can suppress prices for years.

Avoiding these outcomes is exactly why strong financial management practices matter so much for community associations. The board's financial decisions today determine what the neighborhood looks like, and what it's worth, five and ten years from now.

How Boards Can Improve Their Reserve Funding Position

If your HOA's reserve fund is underfunded, the path forward isn't complicated, but it does require discipline and honest communication with homeowners.

The first step is knowing exactly where you stand. If you don't have a current reserve study, get one. You cannot build a funding plan around guesswork. A reserve study gives you a defensible, professionally prepared baseline that the board can share with homeowners to explain why changes are needed.

The second step is building a catch-up plan into your annual budget. This usually means gradually increasing the reserve contribution line in the budget over several years rather than trying to close the entire gap at once. Gradual increases are easier for homeowners to absorb and easier for the board to defend. Reviewing common annual budget pitfalls can help boards avoid making the underfunding problem worse while they work to fix it.

The third step is keeping homeowners informed. Boards that communicate openly about reserve health, what the funding gap is, what the plan is to address it, and what the risks are if it isn't addressed, tend to get more cooperation when dues adjustments are needed. Homeowners are more accepting of gradual increases they understand than sudden assessments they didn't see coming.

One of the most common mistakes boards make is treating reserves as a line item to cut when the budget gets tight. This is exactly the kind of thinking that leads to the budget myths that cause long-term problems for HOAs. Reserves aren't optional savings. They're the financial foundation that keeps the community functioning.

Keeping Reserve Information Accessible to Homeowners

One of the simplest things a board can do to build trust around reserve health is make the information easy to find. When homeowners can access the current reserve study, see the percent funded figure, and understand what projects are coming up, they're less likely to feel blindsided and more likely to support the decisions the board needs to make.

Posting reserve study documents, annual budgets, and financial updates on your HOA's community website removes friction and signals that the board has nothing to hide. It also gives prospective buyers and their agents easy access to the information they're going to look for anyway, which reflects well on the community.

Neighborhood.online gives boards a central place to store and share these documents, communicate financial updates, and keep the community informed throughout the year. When financial transparency is easy, it tends to happen more consistently.

Conclusion

There's no single magic number that every HOA should hit in reserves. But there is a clear framework for evaluating whether your community is on solid ground: understand your percent funded figure, know what's coming up in your replacement schedule, and make sure your annual contribution rate is moving you in the right direction.

A percent funded above 70% is the target. Below 30% is a warning that action is needed. And anywhere in between is a call to have an honest conversation with your board and your homeowners about the plan to get stronger.

The boards that handle this well aren't necessarily the ones with the most money. They're the ones that plan honestly, communicate clearly, and make consistent decisions year after year. That's what financially healthy communities look like, and it's entirely within reach for most HOAs.

For a deeper look at how to structure the accounts that hold these funds, see our guide to maintaining separate accounts for operating and reserve funds.

Not Sure Which Expenses Belong in Reserves?

Many HOA budgets run into trouble because operating expenses and reserve expenses get mixed together.

Our Operating vs. Reserve Fund Classifier spreadsheet shows where common HOA expenses belong so boards can budget more accurately and avoid reserve shortfalls.

Topics

Frequently Asked Questions About HOA Reserves

Not exactly. Reserves refer specifically to the funds an HOA sets aside for the future repair and replacement of major common area components, things like roofs, parking lots, pool equipment, and fencing. It is a separate pot of money from the operating fund, which covers the HOA's day-to-day expenses. An HOA may have a healthy operating balance and still be significantly underfunded in reserves, which is why the two accounts should always be evaluated separately.

The most widely used rule of thumb is the percent funded benchmark. A reserve fund that is 70% funded or higher is generally considered healthy. Below 30% is a warning sign that the community is at risk of deferred maintenance, surprise special assessments, or difficulty attracting buyers who need conventional financing. Most reserve professionals aim for a stable, upward funding trajectory rather than a fixed target number, since the right amount depends on the age of your components and what replacements are coming up.

The right number is specific to your community and can only be determined by a reserve study. A reserve study catalogs every major component the HOA is responsible for, estimates remaining useful life, projects replacement costs, and builds a funding plan around those timelines. A community with a 30-year-old roof due for replacement in two years needs very different reserves than a community where no major projects are due for a decade. There is no universal dollar amount that applies across all HOAs.

70% funded or higher is the standard benchmark for a healthy HOA reserve fund. At this level, the community has enough saved relative to the age and condition of its components to handle anticipated replacements without financial surprises. Between 30% and 70% is considered fair but requires a clear plan to improve. Below 30% is considered poor and puts the community at real risk of special assessments or deferred maintenance.

Most reserve specialists and community association professionals recommend targeting at least 70% funded. Some lenders and state regulations set their own minimums. Fannie Mae and Freddie Mac require condominium associations to allocate at least 10% of their annual budget to reserves as a condition for conventional mortgage approval in the community. FHA has similar requirements. Even where no legal minimum applies, staying at or above 70% funded is the best protection against special assessments and declining property values.

Roof costs vary widely depending on the size of the building, roofing material, and local labor rates. For a typical single-family home in an HOA, roof replacement can run anywhere from $8,000 to $20,000 or more. For larger common area buildings or condominium roofs covering multiple units, replacement costs often range from $50,000 to several hundred thousand dollars. HOAs should not rely on general estimates. A reserve study will include a site-specific projection for each roof the HOA is responsible for, adjusted for local costs and inflation over the replacement timeline.

Condominium reserves are funds set aside by a condominium association to pay for the future repair and replacement of major shared components. These typically include roofs, elevators, parking structures, pool equipment, hallways, and building systems that all unit owners share. Because condominium unit owners do not individually own or maintain these components, the association collects reserve contributions through monthly dues and holds the funds on behalf of the community. Many states have specific laws governing how condominium reserves must be funded and reported.

A common guideline is to keep total housing costs, including mortgage, property taxes, insurance, and HOA dues, at or below 28% to 30% of your gross monthly income. HOA dues vary widely, from under $100 per month for small communities to several hundred dollars or more for communities with extensive amenities. Beyond the monthly dues, it is worth reviewing the HOA's reserve fund health before buying. An underfunded HOA is more likely to issue a special assessment, which is an additional one-time charge on top of regular dues. Factoring in that risk is part of understanding what a home in a particular HOA will actually cost you over time.

A reserve fund study is typically conducted by a licensed reserve specialist or engineer, not by the board itself. The process involves a physical inspection of all major components the HOA is responsible for, an assessment of each component's remaining useful life and projected replacement cost, and the development of a multi-year funding plan. The result is a written report the board can use to set annual reserve contributions. Most professionals recommend a full study with a site visit every three to five years and an annual financial update in between.

Most reserve professionals recommend a full reserve study with a physical site inspection every three to five years. Between full studies, an annual financial update, which is a paper review without a site visit, is recommended to adjust for contributions made, interest earned, and any changes in projected costs. If your HOA has never had a reserve study, or if the last one is more than five years old, it should be treated as a priority. A study that is several years out of date may significantly underestimate current replacement costs, especially given construction cost increases in recent years.

If you want simple, modern, and free to start, you are in the right place.

We run your community.

Set up a complete community platform in under an hour. No developer required. No credit card needed. No accounting degree required.