Build Your HOA Website Free

Neighborhood.online gives your community a modern website, document storage, and communication tools in minutes. No technical skills required.

How to Build a Strong Reserve Contribution Strategy

Most HOA boards know they need a reserve fund. Fewer know how much to actually put into it each month. That gap, small as it seems on paper, is where special assessments are born. A solid reserve contribution strategy is what separates boards that handle major repairs without drama from boards that have to call an emergency meeting and tell homeowners they owe $3,000 by the end of the quarter.

If your board has already done the work of forecasting your financial needs over the next three to five years, this is the natural next step. Now you figure out how to actually fund what you found.

What a Reserve Contribution Strategy Is

A reserve contribution strategy is simply your HOA's plan for how much money to set aside each month, and why. It answers two questions: how much do we need in reserves to be in good shape, and how do we get there from where we are right now?

Your reserve fund is meant to cover major repairs and replacements to shared property. Think roofing, paving, pool equipment, exterior paint, elevators, fencing, and similar long-lived assets. These costs are predictable in the sense that every asset has a lifespan. The uncertainty is not whether you will need to replace the roof. The uncertainty is whether you will have the money ready when it happens.

A contribution strategy takes the output of a reserve study (a list of components, their remaining useful life, and their estimated replacement cost) and works backward to figure out what you need to be depositing today. It is not a guess. It is a plan.

Why This Matters for HOA Boards

Underfunded reserves are one of the most common and most preventable financial problems HOAs face. They tend to develop slowly, over years of boards making small, well-intentioned decisions to keep dues low. Then a major expense arrives and the money simply is not there.

The consequences are real. Your board may have to issue a special assessment, which creates immediate friction with homeowners and can damage trust in the board. You may need to take out a loan, which adds interest costs and takes years to pay off. In some cases, boards defer the repair entirely, which almost always makes the eventual cost higher.

There is also an impact on property values. When a buyer's lender reviews an HOA as part of a mortgage application, reserve health is one of the things they look at. A community with reserves funded below 30 percent is considered a financial risk by many lenders. Some loan types will not approve purchases in communities with severely underfunded reserves. That affects every homeowner's ability to sell, not just the board's budget.

The good news is that a strong contribution strategy, started today, starts fixing the problem immediately. You do not need to be fully funded overnight. You need a credible, documented plan for getting there.

The Three Reserve Funding Models

There are three main approaches boards use when deciding how much to contribute. Each represents a different philosophy about risk, dues stability, and long-term planning. Understanding all three helps your board make an informed choice rather than just copying what the previous board did.

The fully funded model means your reserve balance equals what your reserve study says it should be at any given point in time. If your study says your community's reserve fund should hold $400,000 today based on the age and condition of your assets, you aim to have $400,000. This approach offers the strongest financial protection and the clearest story to tell lenders and prospective buyers. The tradeoff is that getting to fully funded from a low starting point may require meaningful dues increases or a phased ramp-up period.

The threshold funded model sets a floor rather than a target. Your board decides on a minimum balance you will never let the fund drop below, typically enough to cover your two or three most expensive near-term projects. This approach is more flexible and often more politically manageable, especially in communities where dues increases are contentious. The risk is that it requires accurate forecasting. If an unexpected major expense hits at the same time as a planned one, you can find yourself below the threshold before you realize it.

The baseline funded model aims to keep your reserve balance above zero at all times, without targeting a specific percentage of fully funded status. This is the most minimal approach and is generally considered acceptable only as a short-term strategy while a board works toward a stronger funding position. Boards relying on baseline funding for years at a time are taking on meaningful financial risk.

Most reserve professionals and financial advisors recommend moving toward fully funded as a long-term goal, with threshold funding as a reasonable interim position for communities that are catching up.

How to Build Your Contribution Strategy Step by Step

You do not need a finance background to build a solid contribution plan. You need the right information and a willingness to make a few straightforward decisions.

Start with your reserve study. If you do not have one, or yours is more than three years old, updating it is the first priority. The study gives you the raw numbers: a list of components, their current condition, their expected remaining useful life, and their estimated replacement cost. Without this, any contribution number you pick is essentially a guess.

Next, calculate your percent funded. This is your current reserve balance divided by what the reserve study says your fully funded target is, expressed as a percentage. A community with $150,000 in reserves and a fully funded target of $500,000 is 30 percent funded. Anything below 70 percent is generally considered underfunded. Below 30 percent is considered critically underfunded by most lenders and reserve analysts.

From there, work with your reserve study provider or treasurer to model a funding ramp. A ramp is simply a plan to increase contributions gradually over several years until you reach your target funding level. For example, a board that is currently contributing $800 per unit per year might model a plan that increases contributions by $75 per unit per year for five years. That kind of gradual increase is much easier for homeowners to absorb than a sudden jump, and it still moves the needle meaningfully.

Build the contribution into your annual budget as a fixed line item, not an afterthought. One of the most common budget mistakes boards make is treating reserve contributions as flexible spending that can be reduced when operating costs run high. Reserve contributions are not optional. They are deferred maintenance you are paying for in advance. Cutting them today creates a larger problem tomorrow.

Finally, review your contribution plan every year alongside your reserve study update. Costs change. Conditions change. A roof that was expected to last ten more years might show signs of accelerated wear at year seven. Your funding plan needs to keep up with reality.

Avoid the Most Common HOA Budget Mistakes

Many HOA financial problems come from small budgeting mistakes that go unnoticed for years — underfunded reserves, outdated vendor costs, or missed insurance increases.

Our Annual Budget Pitfalls Checklist helps boards quickly review their financial planning and catch the issues that most often lead to special assessments.

Finally, review your contribution plan every year alongside your reserve study update. Costs change. Conditions change. A roof that was expected to last ten more years might show signs of accelerated wear at year seven. Your funding plan needs to keep up with reality.

How Technology Helps You Stay on Track

One of the practical challenges with reserve contribution planning is keeping the board aligned and keeping homeowners informed. When contribution levels increase, homeowners want to understand why. When a major repair is coming up, the community needs context, not a surprise.

Neighborhood.online makes it easier to manage both sides of that equation. Financial documents including your reserve study, annual budget, and contribution history can be stored in one place where board members and homeowners can access them any time. When dues increase to reflect a higher reserve contribution, the board can use the communication tools to send a clear, calm explanation to every homeowner at once, referencing the documents that support the decision.

That kind of transparency builds trust. Homeowners who understand why contributions are increasing are far more likely to accept the change than homeowners who receive a new dues statement with no context. Good communication does not make the math easier, but it does make the conversation a lot smoother.

A Few Numbers to Know

If your board is trying to get oriented quickly, here are some general benchmarks that reserve professionals commonly reference. These are starting points for conversation, not substitutes for a proper reserve study.

A percent funded level of 70 percent or above is generally considered healthy. Between 30 and 70 percent indicates moderate risk and suggests a funding ramp is overdue. Below 30 percent is a serious concern that typically warrants an immediate plan to increase contributions, potentially including a temporary special assessment to build the balance back up while the ramp takes effect.

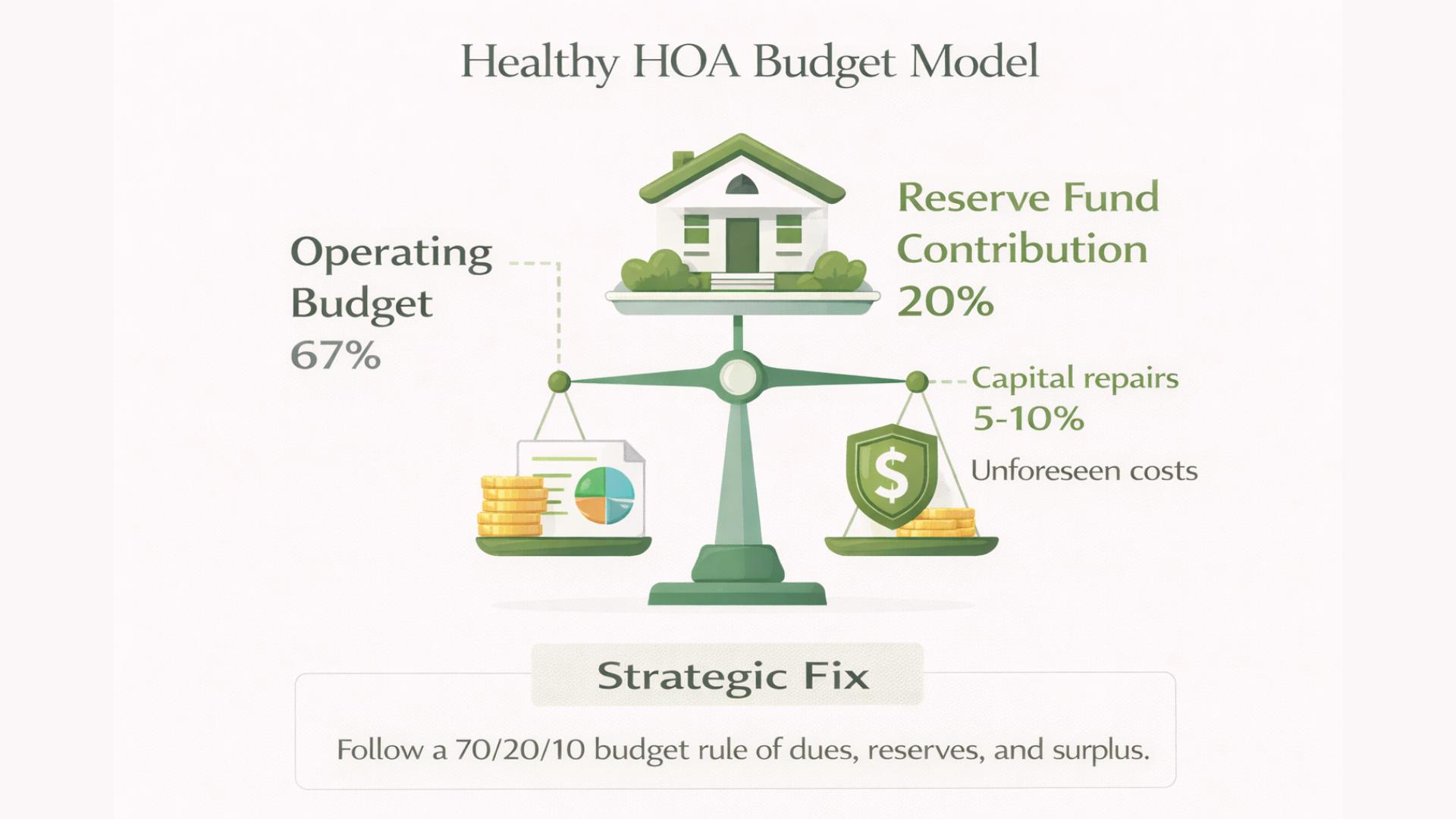

Reserve contributions as a share of total HOA dues vary widely depending on the age and complexity of a community. Newer communities with fewer aging assets might allocate 15 to 20 percent of dues to reserves. Older communities with significant infrastructure nearing end of life might need to allocate 30 to 40 percent or more. Your reserve study will tell you what your specific community needs.

Building the Plan Is the Hard Part

Once your contribution strategy is documented and built into your budget, the ongoing work is mostly about consistency. Contribute what the plan says. Update the plan annually. Communicate changes clearly to homeowners. Resist the pressure to cut reserve contributions when the operating budget gets tight.

That last part is where many boards struggle. When dues are already a sensitive topic and operating costs spike, it is tempting to reduce reserve contributions as the path of least resistance. Understanding the difference between operating and reserve funds helps boards hold that line, because the two serve completely different purposes and should never be traded off against each other.

A well-funded reserve is one of the most concrete things a board can do for its community. It protects property values, prevents financial emergencies, and gives homeowners confidence that the people running their neighborhood have a real plan. That is worth the effort of building it properly.

Avoid the Most Common HOA Budget Mistakes

Many HOA financial problems come from small budgeting mistakes that go unnoticed for years — underfunded reserves, outdated vendor costs, or missed insurance increases.

Our Annual Budget Pitfalls Checklist helps boards quickly review their financial planning and catch the issues that most often lead to special assessments.

Topics

If you want simple, modern, and free to start, you are in the right place.

We run your community.

Set up a complete community platform in under an hour. No developer required. No credit card needed. No accounting degree required.