How to Read an HOA Financial Statement (Beginner-Friendly Guide)

Understanding Special Assessments

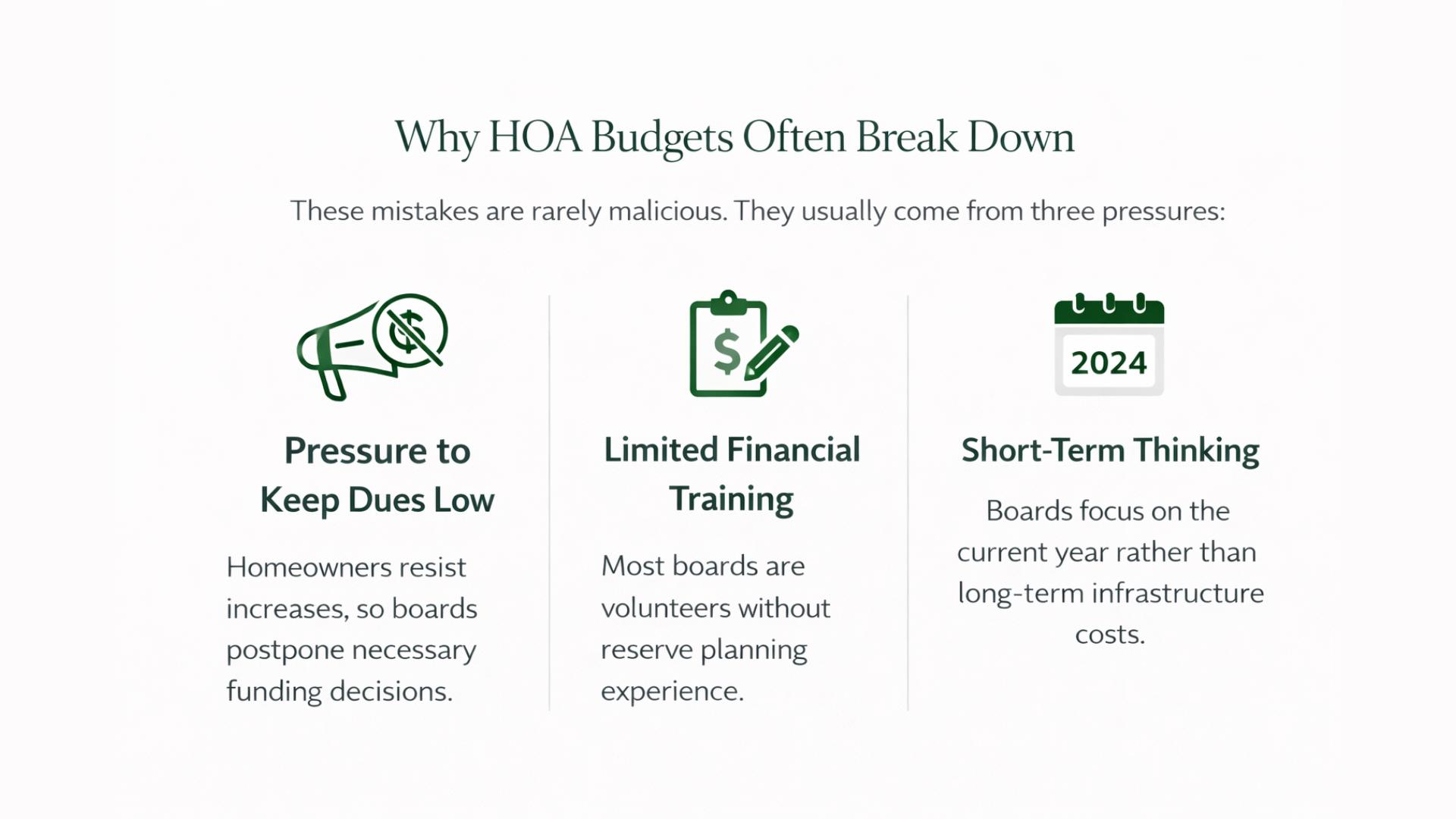

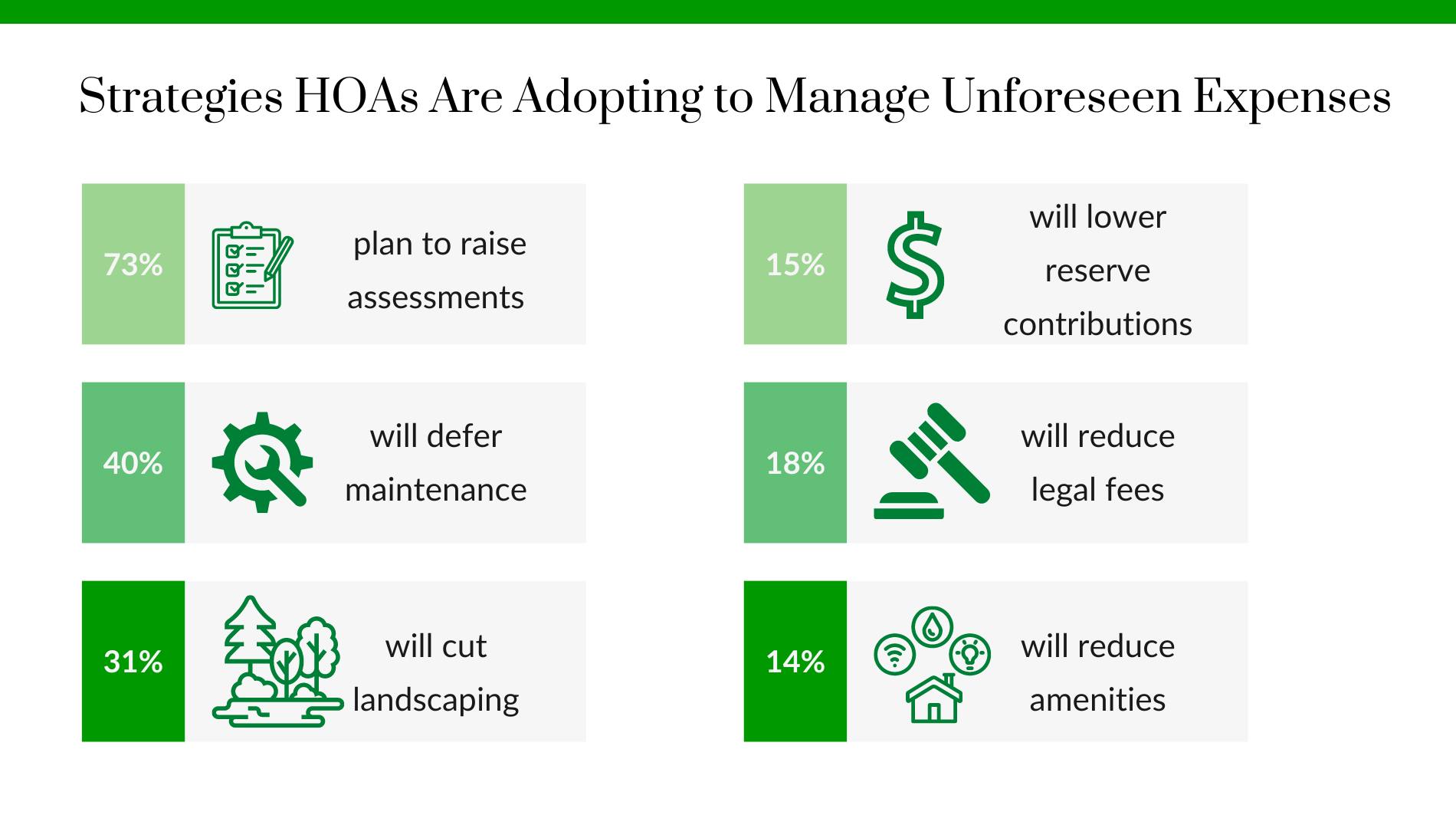

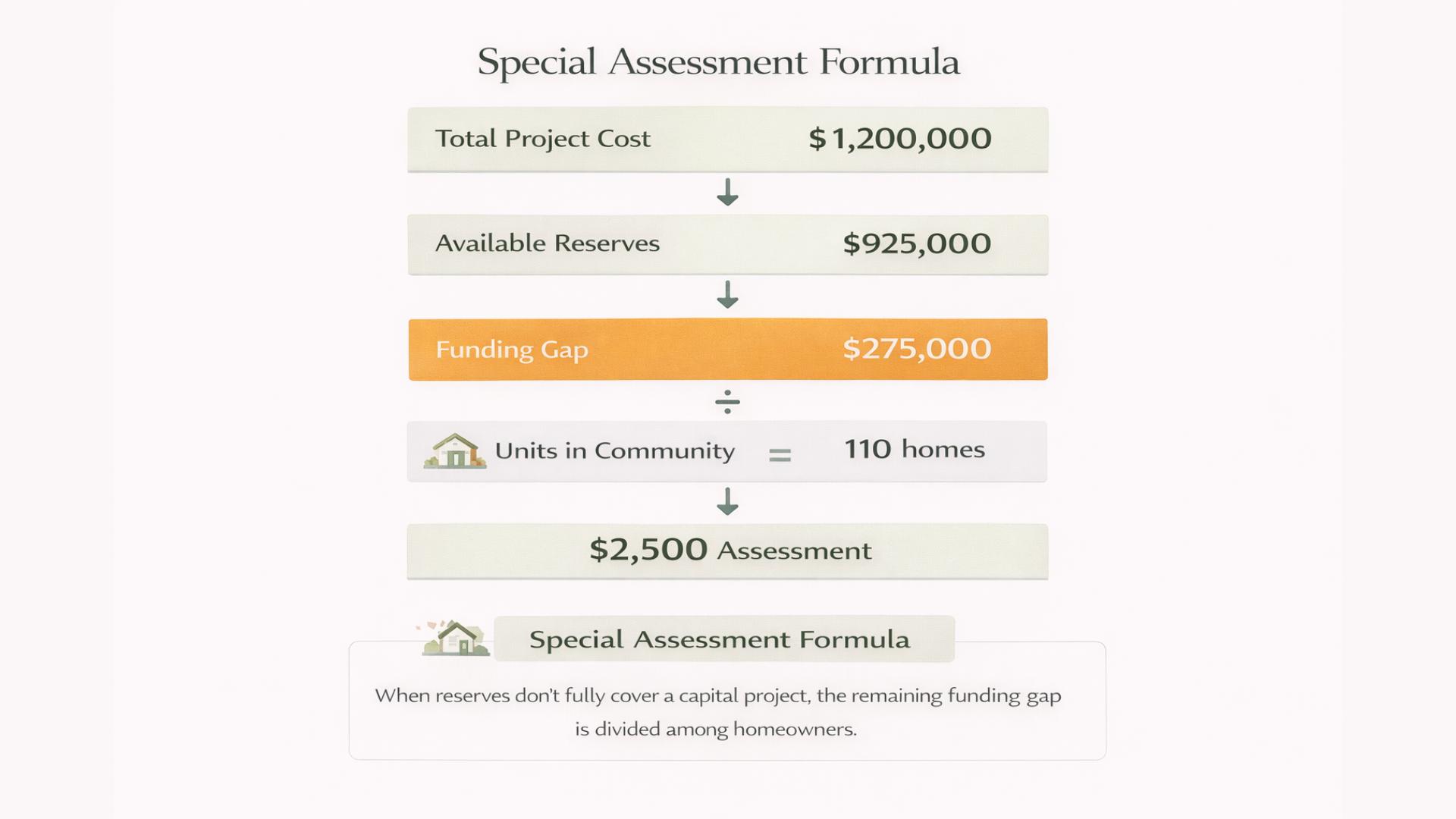

Special assessments often feel sudden and confusing to homeowners. In reality, they usually come from predictable financial gaps.

Our Special Assessments Explainer breaks down what causes them, how they’re calculated, and how communities can avoid them with better planning.

If you have ever opened an HOA financial report and felt immediately lost, you are in good company. Most HOA board members are volunteers with full-time jobs and busy lives. Reading an HOA financial statement is not something most people learned how to do, and the reports themselves are not always designed with a non-accountant in mind. But understanding your financial statements is one of the most valuable skills a board member can develop, because these reports are where the real story of your community's financial health lives.

The good news is that you do not need a background in finance to read them well. You need to know what the key reports are, what each one is telling you, and where to look for the signals that matter most. This guide walks through all of it in plain language.

Why HOA Financial Statements Matter More Than Most Boards Realize

Financial statements are not just paperwork to approve at a board meeting. They are the primary tool boards have for understanding whether the community is financially healthy, whether it is heading toward trouble, and whether the decisions being made today are setting the HOA up for stability or strain down the road.

A board that reviews financial statements carefully every month catches problems early, when they are still manageable. A board that glosses over them, or simply approves them without really understanding what they show, often finds out about financial problems much later, when the options for solving them are more limited and more expensive. When that understanding is combined with strong HOA financial transparency practices, financial reports also become a tool for communicating clearly with homeowners rather than just a document the board keeps to itself.

The Four Core HOA Financial Reports

Most HOA financial packages include four main reports. Each one covers a different dimension of the association's finances, and together they give a complete picture of where things stand.

The balance sheet is the starting point. It shows your HOA's financial position at a single point in time, listing everything the association owns (assets like cash, reserve fund balances, and amounts owed by homeowners) alongside everything it owes (liabilities like unpaid vendor invoices or outstanding loans). The difference between those two figures is the association's equity, or net position. A healthy balance sheet shows assets comfortably exceeding liabilities, with reserve funds growing as planned.

The income statement, sometimes called the profit and loss report, covers a period of time rather than a single date. It tracks all the money that came into the association (primarily dues, but also late fees, rental income from shared facilities, or other sources) against all the money that went out in operating expenses. The most important thing to look for here is the comparison between budgeted amounts and actual amounts. If landscaping was budgeted at $2,400 for the month and the actual cost came in at $3,100, that variance deserves a conversation. One month of overrun might be explainable. Three months in a row is a trend worth addressing before it compounds.

The cash flow statement tells you how much actual cash is available at a given point in time, which is a different question than whether the budget looks balanced. An HOA can show a surplus on paper and still run into cash flow problems if dues payments are delayed, a large vendor invoice comes due before the next assessment cycle, or an unexpected repair needs to be paid immediately. Boards that monitor cash flow regularly are far less likely to be caught short when timing works against them.

The reserve fund report tracks the long-term savings picture. It shows the current reserve balance, the contributions made during the period, and any withdrawals for capital repairs or replacements. The key question here is whether reserve contributions are happening as planned and whether the balance is growing in line with what your reserve study recommends. If you are not familiar with how reserve funds work separately from operating funds, the guide to reserve funds explained in simple terms is a helpful place to start.

What to Actually Look for When You Sit Down to Review

Reading a financial statement well does not mean analyzing every line item in detail. It means knowing where to focus your attention so you can spot the signals that matter. There are four areas worth making a habit of checking every month.

Budget versus actual is the most immediately useful comparison in any financial package. For every major expense category, you want to know whether actual spending is tracking close to what was planned, running ahead of budget, or consistently falling short in a way that might signal deferred spending. Small variances are normal. Recurring variances in the same category, month after month, usually mean the budget needs to be revisited or a cost has changed and the board has not caught up to it yet.

Reserve contributions deserve a specific check every single month. It is surprisingly common for reserves to be underfunded simply because contributions were skipped or reduced during a tight month without a formal board decision to do so. Skipping reserve contributions is one of the fastest ways to create a future special assessment situation. If contributions are on track and growing as the reserve study recommends, that is a healthy sign. If they are lagging, the board needs to understand why and have a plan.

Delinquencies are worth reviewing on the income side. Unpaid dues are a quiet but real threat to HOA finances, because they reduce the revenue the association is counting on to cover operating expenses and reserve contributions. A small number of delinquent accounts in a large community may be manageable, but a rising delinquency trend is worth flagging early. The guide to collecting assessments and handling delinquencies covers the practical steps boards can take when this becomes an issue.

Cash position is the final check. After reviewing income, expenses, and reserves, make sure the operating account has enough cash to comfortably cover the next four to six weeks of expected expenses without needing to pull from reserves. If the margin feels thin, that is worth discussing before it becomes a problem rather than after.

Common Mistakes Boards Make When Reviewing Financials

The most common mistake is reviewing totals without looking at trends. A monthly net surplus can mask the fact that a particular expense category has been running over budget for four months straight. Looking at individual line items and comparing them to the same period in prior years, not just to the current month's budget, gives a much clearer picture of what is actually happening.

A close second is treating reserve balances as a general emergency fund. Reserves are designated for specific capital repairs and replacements identified in the reserve study. Using them for operating shortfalls without a formal board decision and a plan to replenish them creates compounding problems. The board ends up underfunding both the operating budget and the reserve fund simultaneously, which tends to end with a special assessment.

Boards that want to go deeper on the warning signs embedded in financial reports will find the guide to warning signs to look for when reviewing financials a useful companion to this one.

How the Right Tools Make Financial Review Easier

Reviewing financial statements is easier when the information is organized consistently and accessible to the full board, not just the treasurer. Many boards still manage financial documents through email threads and shared drives that are difficult to navigate and easy to let fall out of date. When board members cannot easily pull up last month's income statement to compare it to this month's, the quality of financial review suffers.

Platforms like Neighborhood.online give boards a centralized place to store and share financial documents, so every board member can review reports before a meeting and homeowners can access the information they are entitled to see without having to ask. That accessibility supports both better board decisions and the kind of clear treasurer reporting that keeps the full community informed.

Understanding Special Assessments

Special assessments often feel sudden and confusing to homeowners. In reality, they usually come from predictable financial gaps.

Our Special Assessments Explainer breaks down what causes them, how they’re calculated, and how communities can avoid them with better planning.

Financial Literacy Is One of the Best Investments a Board Can Make

No one expects a volunteer board member to become a CPA. But a board that understands its financial statements, knows what healthy looks like, and can spot the early signs of trouble is a board that makes better decisions for everyone in the community.

Start by committing to review all four reports every month, not just the summary totals. Ask questions when something does not make sense. Build the habit of comparing actuals to budget and this year to last year. Over time, reading a financial statement will shift from something that feels unfamiliar and overwhelming to something that takes twenty minutes and tells you exactly where your community stands.

That knowledge is what allows boards to plan ahead, communicate confidently, and avoid the kind of financial surprises that tend to create conflict and erode trust. It is worth the effort to build that habit now, before a problem forces the issue.